The AI Control Grid: Banking, Data Centres, and the Open-Air Prison Being Built Around Us

How AI infrastructure, digital finance, regulatory capture, and centralized systems are quietly converging into a new model of control.

This isn’t just about Iran, China, AI, or war. It’s about who controls energy, infrastructure, information, food, finance… and ultimately people. Whether you agree or disagree, this may be the most important two hours you spend on YouTube this year.

This guy might know a thing or 2… Richard A. Werner is an Oxford- and LSE-educated economist, professor of banking and finance, and internationally recognized expert on central banking and monetary policy. He is best known for coining the term “Quantitative Easing” in 1995 and for his bestselling book Princes of the Yen. Over a 30-year career, Werner has advised governments, central banks, pension funds, and major global financial institutions. His research on banking, credit creation, and financial crises has become some of the most widely downloaded academic work in the world, making him a leading voice on economic reform and the global economy.

BUCKLE UP FOLKS…CLICK ON THE IMAGE BELOW

What struck me most about this interview was not simply the discussion of war, propaganda, or global power struggles. It was the deeper warning buried underneath it all: the battle for control is no longer just about oil fields, shipping lanes, or military dominance. It is increasingly about control of infrastructure itself … digital infrastructure.

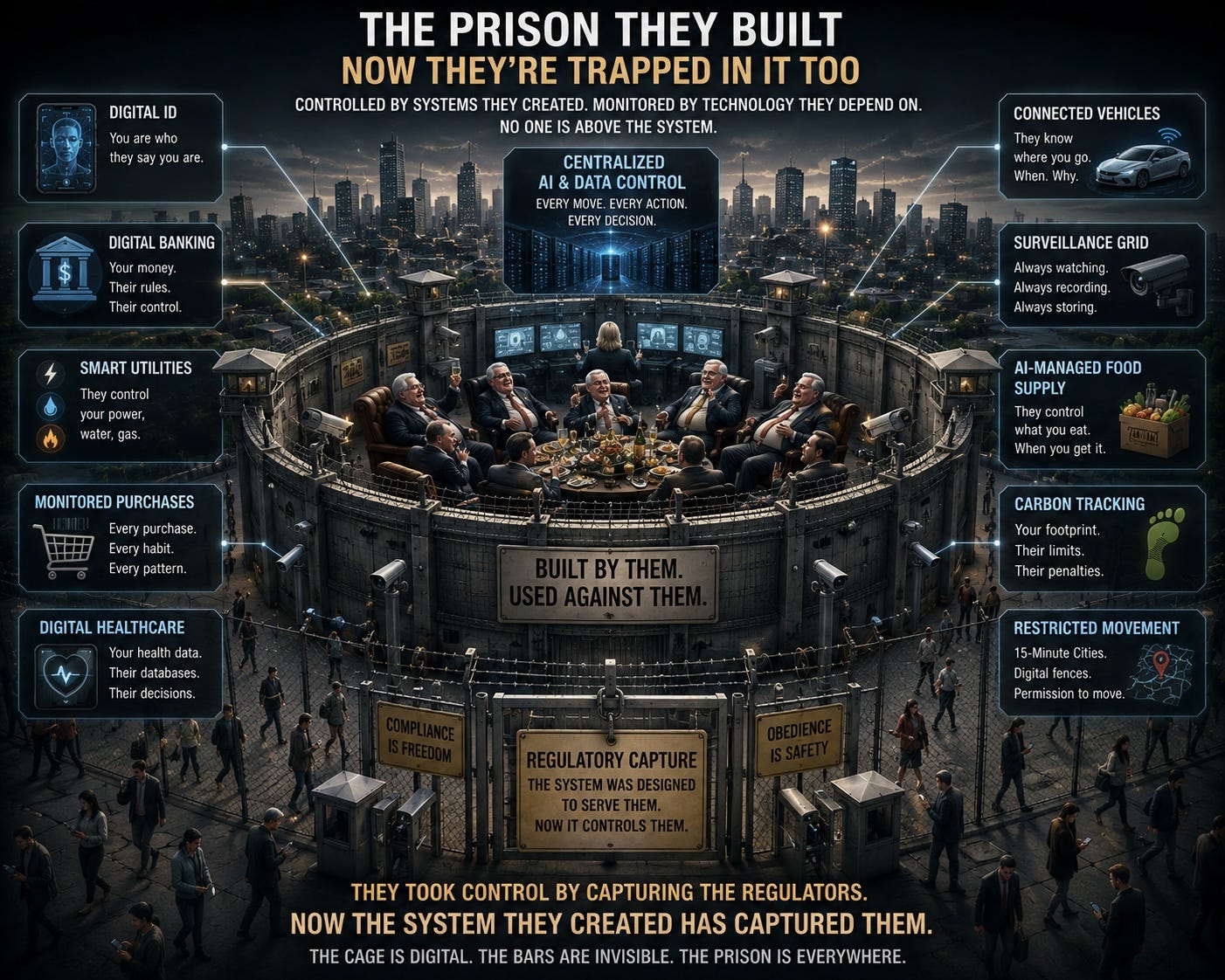

AI data centres are being presented to the public as harmless symbols of “innovation” and “progress.” But these facilities are far more than giant computer warehouses. They are rapidly becoming the backbone for real-time surveillance, smart grids, digital banking, AI-managed logistics, predictive policing, automated agriculture, digital identity systems, facial recognition, and eventually entire interconnected “smart” societies.

None of this works without massive centralized computing power.

That is why governments and corporations are racing to secure:

electricity,

water,

transmission corridors,

fibre infrastructure,

carbon capture systems,

and AI partnerships.

AI does not run on “the cloud.” It runs on physical infrastructure, that being, land, energy, water, minerals, and centralized control systems.

The interview draws historical parallels between old empires controlling railways, shipping routes, oil corridors, and financial systems, and the modern race to dominate AI infrastructure and global digital systems.

History shows that whoever controls infrastructure ultimately controls nations.

Railways changed civilization. Oil changed civilization. Central banking changed civilization. The internet changed civilization.

AI infrastructure may change civilization more than all of them combined.

And this is where people need to stop dismissing concerns about 15-minute cities, digital currencies, and centralized AI systems as isolated issues.

Because they are not isolated. They are converging.

IMAGINE a future where your identification is digital, your banking is digital, your vehicle is connected, your utilities are “smart,” your purchases are monitored, your healthcare is digitized, your food supply is AI-managed, your carbon footprint is tracked, and your movement is increasingly tied to centralized systems.

WAIT SAY WHAT? are we there yet?

Now connect all of that to AI-driven infrastructure capable of monitoring, analyzing, and responding to human behaviour in real time.

At that point, freedom itself becomes conditional on system access.

And then comes the banking question that almost nobody in Canada is talking about.

Until very recently, the sunset provision inside Canada’s Bank Act stated that federally regulated banks could not continue carrying on business after June 30, 2026 unless Parliament renewed the legislative framework governing Canada’s banking system.

That wording has now quietly been amended, extending the date to June 30, 2033.

Some people immediately dismissed concerns surrounding the clause by claiming, “See? Nothing was ever happening.” But that completely misses the bigger picture.

First, the sunset provision was never proof that all banks would automatically shut their doors on June 30, 2026. The clause functions as a legislative review mechanism requiring Parliament to periodically renew and modernize the legal framework governing Canadian banking.

However, maybe even more importantly, extending the sunset date to 2033 also does not guarantee that banks themselves must remain open, unchanged, or operational until then.

Banks can still fail, merge, collapse under financial stress, lose their charter, move increasingly digital, reduce physical branches, or fundamentally transform long before 2033 arrives.

And that transformation is already happening. Across Canada and around the world we are watching physical bank branches disappear, cash services reduced, banking move online, AI-driven financial monitoring expand, digital verification systems grow, and governments openly discuss Central Bank Digital Currencies (CBDCs), digital identity systems, and programmable finance.

So while some people focus narrowly on the sunset date itself, the more important question may be this: What kind of banking system is being built between now and 2033?

Because banking is no longer just about money. It is increasingly becoming integrated with digital identity, AI systems, real-time surveillance, behavioural analytics, centralized databases, smart devices, and broader digital infrastructure.

That is why the discussion around AI data centres matters so much.

AI infrastructure is not separate from the future of finance. It is the computational backbone that makes large-scale centralized digital systems possible.

A world where freedom itself becomes increasingly dependent on access to the system.

And history shows that centralized systems are rarely built all at once. They are introduced incrementally for convenience, for security, for efficiency, for sustainability, for modernization. One layer at a time.

That is why public awareness matters.

Whether by design, technological limitations, political resistance, economic instability, or growing public skepticism, it is entirely possible that the transition toward a fully integrated digital financial system is proving far more complicated than planners expected.

Perhaps the infrastructure is not fully ready. Perhaps the public is asking too many questions. (No Such Thing). Or perhaps the people building these systems are beginning to realize something history has repeatedly demonstrated: Once centralized control systems are fully built, even the architects of those systems may eventually find themselves trapped inside the machine they created.

Because the surveillance grid does not distinguish between citizen and politician.

The digital control system does not care whether you helped build it.

And the open-air prison eventually closes around everyone.

“He who controls the data centres may eventually control the money, the movement, the food, and the flow of information itself.”

Regulatory capture may enrich and empower a small group for a time, but eventually the machine begins to govern everyone, including those who built it.

And that is the real danger. Because once society hands control of energy, banking, food, transportation, communication, identity, and information to centralized AI-driven systems, humanity itself risks becoming dependent on the very infrastructure that controls it.

The people building this system may believe they are designing the future.

"they were building their own prison too…" in hell.

Is anyone doing a deep dive into the impact of Basel III on Canada and Canadians? https://www.osfi-bsif.gc.ca/en/guidance/guidance-library/liquidity-adequacy-requirements-lar-2027-chapter-2-liquidity-coverage-ratio

Basel III was made by the Bank for International Settlements (BIS). Its essence is in the following: BIS runs the IMF, and this, in turn, runs central banks of all countries. The body of such control is called BCBS – the Basel Committee on Banking Supervision. BCBS outlined transitional arrangements from 2017 to 2028 to provide banks sufficient time to adjust their operations and practices to comply with the new standards.